Imagine checking your credit report only to find a complete stranger’s financial history tangled with your own. This is exactly what a mixed credit file is: a common but devastating credit bureau error that happens when people share similar names or social security numbers. It can affect your credit scores, loan approvals, employment screenings, and overall financial stability.

But the Fair Credit Reporting Act (FCRA) fortunately provides a legal way to deal with this hassle. Under federal law, credit bureaus are strictly required to maintain maximum possible accuracy. But what happens if you dispute the errors and they still fail to fix them? Is it actually possible to take them to court?

To get the details, let’s take a closer look at your legal rights and when a credit bureau may be held liable under the FCRA.

Overview of Mixed File Legal RightsA mixed credit file occurs when credit bureaus negligently merge distinct consumer profiles, severely damaging financial opportunities. Under the FCRA, bureaus must conduct a reasonable 30-day reinvestigation upon receiving a formal dispute, cross-checking personal identifiers rather than relying on automated rubber-stamping. If they fail to segregate the data or properly maintain accuracy, consumers can sue for willful or negligent noncompliance to recover financial damages, emotional distress compensation, and attorney fees. |

What Is a Mixed Credit File Under the FCRA?

A mixed credit file happens when a credit bureau accidentally combines information from two different people into the same credit report. This can occur because of errors in the bureau’s matching system or incorrect information provided by lenders.

A mixed credit file may involve information belonging to another consumer appearing on your credit report, which may consist of:

- Identity Cross-Matching Errors

- Foreign Credit Accounts Attached to Your File

- Credit Activity Contamination

- Score and Risk Profile Distortion

- Profile Fragmentation or Over-Merging (Advanced FCRA Issue)

How Credit Bureaus Are Required to Handle Mixed Credit Report Disputes?

When a mixed credit file happens, credit bureaus are required to fulfill the following obligations:

Conduct a Reasonable Reinvestigation

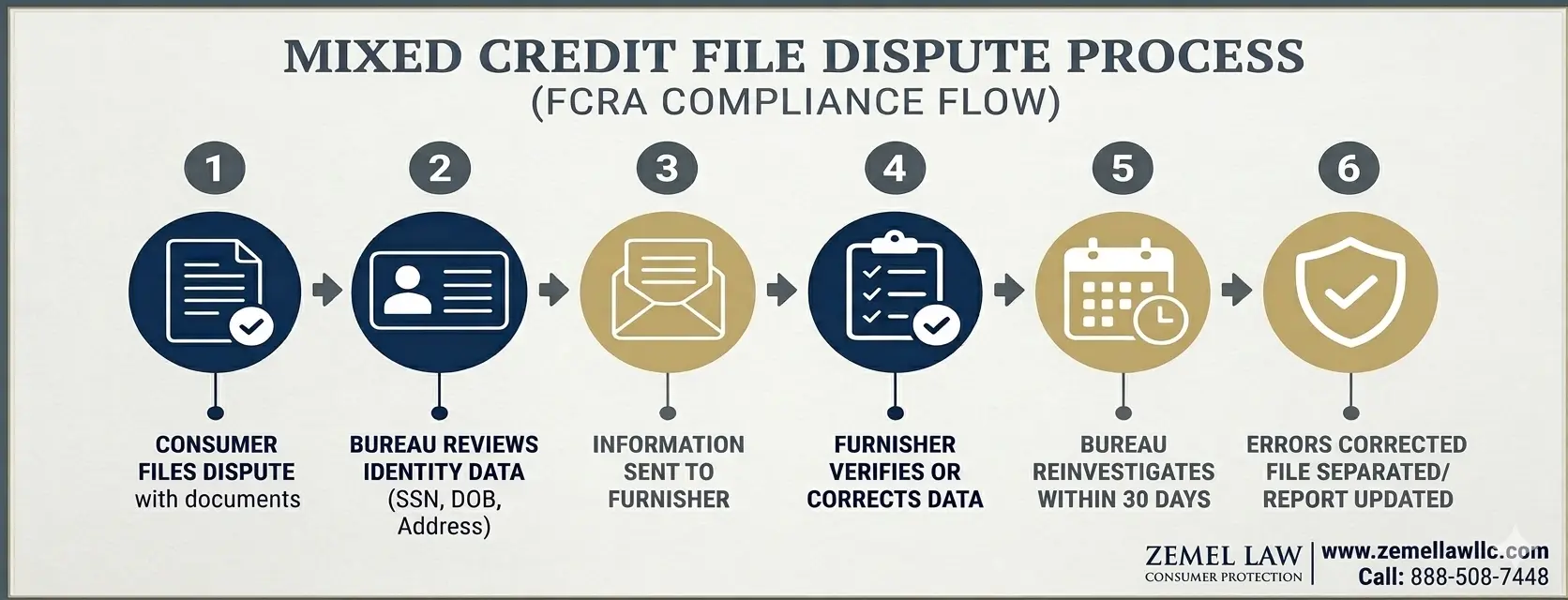

Before a dispute is even filed, FCRA Section 607(b) requires credit bureaus to maintain reasonable procedures to assure maximum possible accuracy. For mixed-file disputes, the bureau may need to examine identifying information such as names, social security numbers, dates of birth, and address histories to determine whether another consumer’s records have been merged into the wrong file.

Review All Relevant Information Provided by the Consumer

Credit bureaus are expected to consider all relevant evidence submitted with a dispute. This may include:

- Government-issued identification

- Social Security documentation

- Proof of address

- Account statements

- Written explanations identifying the mixed-file error

Forward Relevant Dispute Information to Data Furnishers

If the disputed information was reported by a lender, debt collector, or other furnisher, the credit bureau must promptly provide the furnisher with all relevant information received from the consumer. This helps ensure the furnisher can conduct its own investigation into the disputed data.

Correct, Delete, or Update Inaccurate Information

If the investigation reveals that the information does not belong to the consumer, the bureau must correct or remove the inaccurate data from the credit file. Likewise, information that cannot be verified must generally be deleted.

Deleted Information Cannot Be Improperly Reinserted

Once mixed-file information is removed, the bureau must maintain procedures to prevent improper reinsertion. Reappearing accounts generally require proper verification and compliance with the FCRA’s reinsertion requirements before being added back to a report.

Complete the Investigation Within Statutory Deadlines

The FCRA generally requires consumer reporting agencies (Equifax, Experian, or TransUnion) to complete dispute investigations within 30 days of receipt. This period may be extended to 45 days if the consumer submits additional relevant information after the initial dispute, requiring further investigation.

Consumers Must Receive Written Investigation Results

After completing the reinvestigation, the bureau must provide written results to the consumer. If changes were made, the consumer is entitled to receive an updated report and information regarding their rights under the FCRA.

When a Credit Bureau’s Failure Becomes an FCRA Violation

These are some of the violations under the Fair Credit Reporting Act that enable consumers to sue a credit bureau if it fails to fix a mixed credit report. These violations are:

Negligent Noncompliance

A credit bureau is negligent when it fails to take reasonable steps to investigate or correct errors after being properly notified.

In mixed file cases, negligence that comes under FCRA violation may include:

- Ignoring repeated disputes about identity mix-ups

- Failing to correct obvious mismatched personal identifiers

- Relying solely on automated matching systems

- Not reviewing supporting documentation (ID, SSN proof, addresses)

If negligence is proven, consumers may recover:

- Actual damages (credit denial, higher loan costs, emotional distress)

- Attorney’s fees and court costs

Willful Noncompliance

Willful violations are more serious and occur when a bureau knowingly or recklessly disregards its legal obligations. The reasons for this include:

- Repeatedly re-reporting the same incorrect mixed file after disputes

- Ignoring clear identity evidence provided by the consumer

- Systemic failure to correct known file-matching issues

- Using inadequate matching algorithms despite known risks

In willful cases, consumers may recover:

- Statutory damages ($100–$1,000 per violation)

- Punitive damages (in egregious cases)

- Full attorney’s fees

Reasonable Procedures Failure (Core Litigation Theory)

Under Section 1681e(b) of the Fair Credit Reporting Act, consumers may pursue claims by alleging that the bureau’s procedures for assuring maximum possible accuracy were unreasonable under the circumstances.

In mixed credit file cases:

Courts may find evidence of unreasonable procedures where:

- Accounts belong to two distinct consumers but are repeatedly merged.

- The bureau fails to correct structural identity errors after notice of 30 days.

- The same mismatch recurs across multiple reporting cycles.

This shifts the case from “error correction” to systemic compliance failure under FCRA.

Unreasonable or Inadequate Reinvestigation

A bureau can violate §1681i even if it responds within 30 days but conducts an unreasonable investigation. A violation occurs when the credit bureau:

- Does NOT conduct a real investigation under section 1681i

- Simply sends the dispute to the furnisher through an automated system (e-OSCAR)

- Accepts “verified as accurate” without reviewing evidence

- Ignores consumer documents (ID, SSN proof, billing records)

In this situation, consumers can gain:

- Correction/removal of inaccurate accounts

- Credit score restoration

- Compensation for:

- Loan denial

- Higher interest rates

- Emotional distress

- Attorney fees paid by the bureau (successful case)

Inaccurate or Obsolete Reporting (Old or Illegal Data)

Credit bureaus violate the FCRA when they:

- Report debts older than the 7-year reporting limit (section 605(a))

- Keep discharged or settled debts active

- Continue reporting accounts after the legal removal period

- Fail to update corrections from furnishers

Benefits to consumers due to this violation by the credit bureau include:

- Immediate deletion of negative accounts

- Score increase (often significant)

- Eligibility for loans/credit restored

- Possible statutory damages if willful

Attorney AdvertisingNo aspect of this advertisement has been approved by the Supreme Court of New Jersey. Prior results do not guarantee a similar outcome. This article is for informational purposes only and does not constitute legal advice. |

Conclusion

Now, as you have gone through this article, you can clearly see how you can sue a credit bureau under the FCRA if they fail to fix a mixed credit file after a formal dispute. When a credit reporting error causes financial or other harm, seek correction of inaccurate information and pursue available remedies under the FCRA.

At Zemel Law LLC, we help consumers evaluate potential FCRA claims and pursue available remedies when credit reporting errors cause harm. Visit us today to protect your financial future.

FCRA FAQs: Mixed Credit File Claims Against Credit Bureaus

Q1. Do I need to show financial loss to sue for a mixed credit file?

No, emotional distress and credit harm can also support an FCRA claim.

Q2. Is one dispute enough to sue a credit bureau for a mixed file?

In some cases, a single dispute may be sufficient if the credit bureau had clear notice of the error and failed to conduct a reasonable reinvestigation, but the specific facts of each case matter.

Q3. What if all three bureaus report different mixed data?

You can bring separate FCRA claims against each bureau for independent reporting failures.

Q4. Does a temporary correction defeat my FCRA claim?

No, if the mixed data returns, it may still show systemic reporting failure.

Q5. Can a mixed file affect mortgage approval eligibility?

Yes, a mixed credit file can cause mortgage denial or higher interest rates by misreporting credit scores during underwriting.