Personal and financial data play an essential role in life’s different aspects. Whether you’re applying for a loan, a job, or insurance, reports that detail your financial history and personal background can make or break your deals. Two of the most commonly referenced reports are Investigative consumer report vs credit report. But what exactly are these reports, and how do they differ? If you are unaware of both, let’s we’ll break down their differences and explain why understanding them is so important for consumers.

Credit Reports vs Investigative Consumer Reports ExplainedCredit reports and investigative consumer reports are used for different decisions and contain different types of information. Credit reports focus on borrowing and repayment behavior, while investigative consumer reports expand into employment history, criminal records, and personal background details gathered from interviews and public records. |

Credit Report

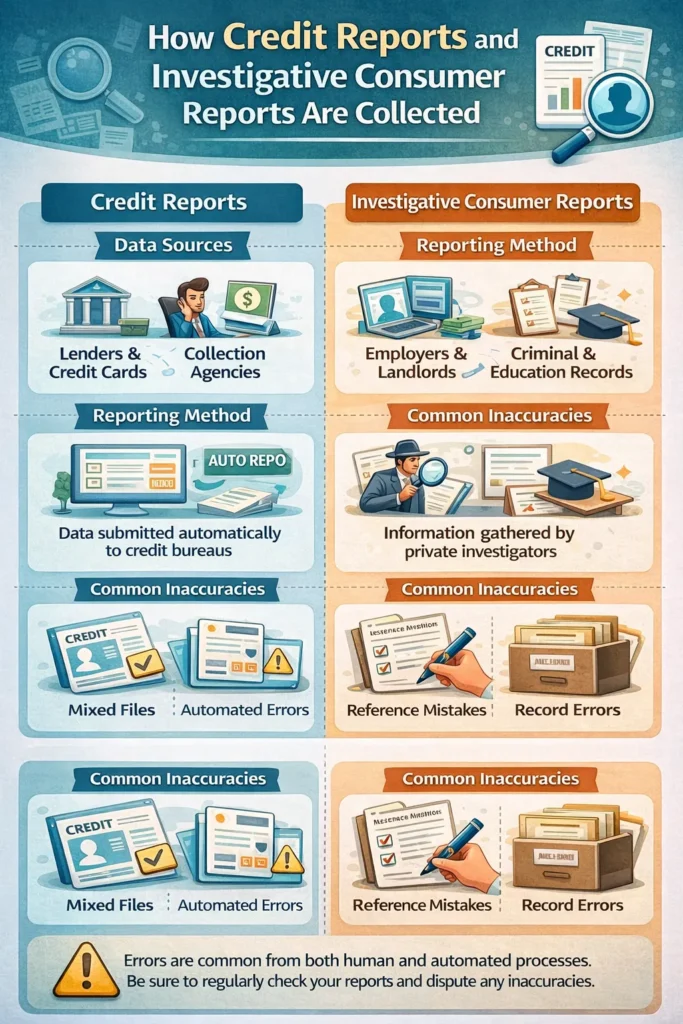

A credit report is a detailed document that shows your credit history and current financial situation, including how well you pay your loans. In the USA, it is compiled by the three major credit bureaus – Equifax, Experian, and TransUnion.

Most individuals have multiple consumer reports credit score because different credit bureaus collect this information from various creditors, such as lenders and credit card companies. Sometimes, these reports are mixed due to inaccuracies in recording or when your data is combined with another person’s information. If you find yourself dealing with inaccuracies, Zemel Law LLC’s mixed credit report attorney can help rectify these issues and protect your financial reputation.

What Information is Included in a Credit Report?

Personal Information

This section includes your name, addresses (both current and past), phone number, Social Security number, date of birth, and employment history.

Accounts

Information about each account will be shown as when it was opened, how much you currently owe, and your payment history (whether you’ve paid on time or missed payments). It also lists details about:

- Revolving Accounts: Credit cards that you can borrow from as long as you pay them back.

- Instalment Accounts: Loans like car or student loans that are paid back in fixed amounts over time.

Inquiries

Credit inquiries are checks made on your credit report, and they come in two types:

- Hard Inquiries: These occur when you apply for new credit, such as a loan, mortgage, or credit card. Hard inquiries may slightly lower your credit score as lenders use this information to assess your creditworthiness. Multiple hard inquiries within a short period can signal risk to lenders.

- Soft Inquiries: Soft Inquiries happen when you check your own credit or when companies perform a credit check for pre-approved offers or background checks. These do not affect your credit score and are only visible to you, not potential lenders.

Collections

Collections include records of any negative entries related to your credit accounts, such as:

- Missed Payments: Any payments that were not made on time.

- Loans Sent to Collections: Accounts that have been forwarded to collection agencies due to non-payment.

- Child Support Payments: Information on overdue child support as provided by local or federal agencies also appears on your consumer reports credit score and remains there for up to seven years.

Public Records

- Liens: Legal claims against your property due to unpaid debts.

- Foreclosures: Instances where your property was repossessed due to non-payment of the mortgage.

- Bankruptcies: Bankruptcies generally remain on your credit report for seven to ten years, depending on the type. A Chapter 7 bankruptcy is visible for up to ten years, while a Chapter 13 bankruptcy lasts for up to seven years.

- Civil Suits and Judgments: Legal judgments against you that may affect your credit.

Purpose and Usage of a Credit Report

Lender Assessments

Lenders use consumer reports credit score to assess creditworthiness. Positive reports enhance loan approval chances and lower interest rates, while a mixed credit report – which reflects both good and bad credit history – complicates a lender’s decision-making process.

Insurance Premium Determination

Insurers use credit reports to determine premiums for cars and homeowners’ insurance. A good credit score often leads to lower rates, reflecting reduced risk for the insurer.

Credit Card Applications

Credit card companies assess credit reports when you apply, and if you have favorable reports, they help you qualify for better cards and lower interest rates.

Fraud Detection and Error Monitoring

Regularly reviewing credit reports helps detect errors and fraud and allows consumers to address issues quickly and maintain their finances. If you experience significant difficulties, such as persistent harassment from creditors or disputes regarding inaccuracies in your report, a credit harassment attorney can provide valuable legal assistance.

Financial Behavior Insights

Your credit report provides insights into financial behavior, aiding in debt management and planning for future loans.

Investigative Consumer Report

Investigative Consumer Reports (ICRs) provide a more comprehensive view of an individual beyond just credit history. According to the Fair Credit Reporting Act (Section 1681a), an investigative consumer report is defined as “a consumer report or portion thereof in which information on a consumer’s character, general reputation, personal characteristics, or mode of living is obtained through personal interviews with neighbors, friends, or associates of the consumer reported on or with others with whom he is acquainted or who may have knowledge concerning any such items of information.

Similarly, California Civil Code Section 1786.2 outlines that investigative credit report ICRs include such information acquired through any means, excluding specific factual details related solely to credit records.

Key Components of an Investigative Consumer Report

Credit Information

Similar to credit reports, consumer investigative report include credit histories, but they are just one part of the report. It includes an individual’s credit score and detailed credit history, such as:

- Credit Accounts: Information on credit cards, mortgages, and loans, including payment history and outstanding balances.

- Credit Inquiries: Records of institutions that have requested the individual’s credit report in the past.

- Delinquencies: Instances of late payments or defaults.

Criminal Background

The criminal history section provides insights into any past legal issues, including:

- Arrests and Convictions: Details of any charges, convictions, or pending legal matters.

- Sex Offender Status: In some cases, reports may include information about registration as a sex offender.

Employment History

- Past Employers: Names, addresses, and employment dates of previous employers.

- Job Titles and Responsibilities: Information on the roles held by the individual.

Public Records and Additional Insights

Same as investigative credit report, ICRs incorporate a wider range of public records, such as civil judgments and bankruptcies, providing a comprehensive overview of any legal issues. They may also include personal references and feedback from previous employers or colleagues, giving a perspective on a person’s character and work ethic.

Purpose and Usage of Investigative Consumer Reports

Employment Screening

Employers use investigative credit report (ICRs) to assess candidate suitability. They evaluate credit history, criminal records, and employment verification to ensure candidates meet job requirements.

Tenant Screening

Landlords use consumer investigative reports to evaluate potential tenants by assessing financial stability, verifying rental history, and checking criminal backgrounds for safety.

Financial Transactions

Financial institutions rely on consumer investigative reports during loan applications to determine creditworthiness and assess debt-to-income ratios, ensuring responsible lending.

The Bottom Line

While credit report vs consumer report may contain similar information, they serve different purposes. Credit reports focus on your financial history, helping you understand your creditworthiness, while investigative consumer reports provide a broader view of your personal background. If you’re experiencing creditor harassment, both of these reports are valuable, as they offer insights that can help you address this issue. Our knowledgeable creditor harassment attorneys in Washington County are ready to help you protect your rights and find a fair resolution. Contact us today!

FAQs

Q1. Can an employer legally use an investigative consumer report without telling me first?

No. Employers must provide clear disclosure and obtain written authorization before requesting an investigative consumer report, and they must also inform you of your right to request additional details about the investigation.

Q2.Why does my background check show information that never appeared on my credit report?

Investigative consumer reports draw from broader sources such as interviews, public records, and employment verification, which is why they may include criminal or character information not tied to credit activity.

Q3. Can errors in an investigative consumer report affect my job or housing application?

Yes. Inaccurate criminal records, employment history, or personal references can influence employment or housing decisions even when a credit report is accurate.

Q4. Do investigative consumer reports follow the same dispute process as credit reports?

They are governed by the Fair Credit Reporting Act, but disputes may require additional documentation because information can come from interviews or third party records rather than automated credit data.

Q5. Can I request a copy of an investigative consumer report used against me?

Yes. If an investigative consumer report contributed to an adverse decision, you have the right to request a copy and review the sources used to compile it.